When you’re prescribed a biologic drug for conditions like rheumatoid arthritis, Crohn’s disease, or psoriasis, the cost can be staggering-often over $4,000 a month. That’s where biosimilars come in: nearly identical versions of these expensive drugs, approved by the FDA, and priced 10% to 33% lower. But here’s the catch: even though biosimilars have been around since 2015 and over 70 are now approved, insurance coverage still makes it hard for most patients to actually use them.

Why Biosimilars Should Be Easier to Access

Biosimilars aren’t generics. Generics are chemically identical copies of small-molecule drugs. Biosimilars come from living cells-like proteins or antibodies-and while they’re not exact copies, they’re proven to work the same way, with no meaningful difference in safety or effectiveness. The FDA has approved more than 70 biosimilars as of 2025, but only about 40 are even on the market. Why? Because insurance rules are blocking the way.Take Humira, the best-selling biologic in U.S. history. It costs nearly $5,000 a month. Eight biosimilars have hit the market since 2023, each costing less. But according to a 2024 JAMA Network study, only half of Medicare Part D plans covered any biosimilar version of Humira. The other half? They still only list the original drug. And even when biosimilars are covered, they’re rarely placed on a lower cost tier.

How Tier Placement Blocks Savings

Most insurance plans use a tier system to control drug costs. Tier 1 might be generic pills costing $5. Tier 4 or 5? That’s where biologics land. Patients pay a percentage of the drug’s price-not a flat copay-so if the drug costs $5,000, a 33% coinsurance means you pay over $1,600 a month out of pocket.Here’s the problem: 99% of Medicare Part D plans put biosimilars and the original biologic on the exact same tier. That means if you switch from Humira to a biosimilar, your monthly cost drops from $1,200 to $1,150. A $50 savings? That’s not enough to motivate patients or doctors to change. The Association for Accessible Medicines found that less than 10% of Medicare plans cover insulin biosimilars, even though insulin costs are a major burden for millions.

And it’s not just Medicare. Commercial insurers like UnitedHealthcare, CVS Caremark, and Cigna have been slow to cover biosimilars at all. A 2023 Center for Biosimilars report showed that even with eight adalimumab biosimilars available, some major insurers didn’t cover any of them. Meanwhile, the original Humira stayed on nearly every formulary.

Prior Authorization: The Hidden Gatekeeper

Even when a biosimilar is covered, getting it approved can feel like climbing a mountain. Nearly all insurance plans (98.5%) require prior authorization for both the original biologic and its biosimilar versions. That means your doctor has to submit paperwork proving you’ve tried other treatments first, that your condition is severe enough, and why you need this specific drug.It takes 3 to 14 business days to get approval. During that time, you might be in pain, unable to work, or delaying treatment. A 2024 survey by the Alliance for Patient Access found that 78% of rheumatologists spend 3 to 5 hours a week just filling out prior authorization forms. One case study showed a patient with severe rheumatoid arthritis waiting 28 days for approval because the insurer forced them to try a biosimilar first-even though the patient had already failed multiple other treatments.

And here’s the twist: some insurers require step therapy. That means you have to try the biosimilar-even if your doctor says it’s not right for you-before they’ll approve the original drug. It’s not about safety. It’s about cost shifting. The patient ends up paying more, waiting longer, and getting less effective care.

Why PBMs Are Changing Their Approach

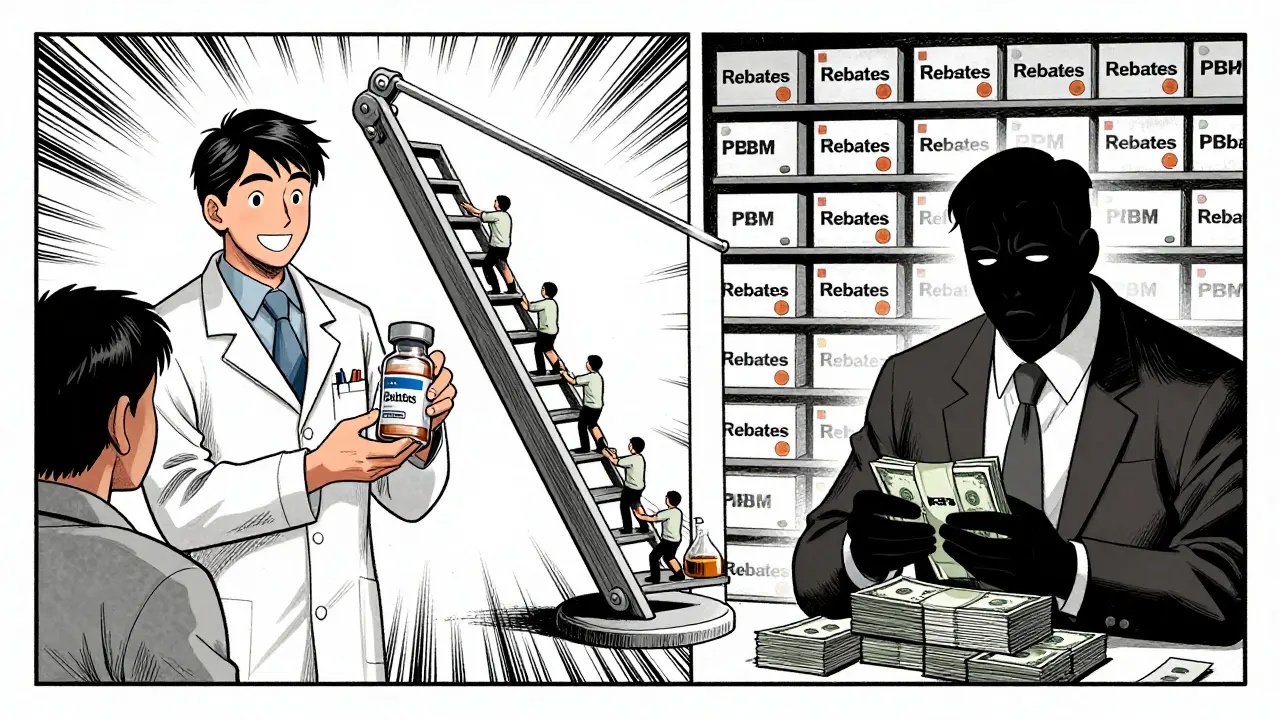

The big middlemen in this system-Pharmacy Benefit Managers (PBMs)-have historically protected brand-name drugs. But in 2025, that’s starting to shift. Express Scripts, OptumRx, and CVS Caremark have all begun removing Humira from their national formularies entirely. Why? Because they’re now forcing patients onto biosimilars instead.Express Scripts, for example, excluded Humira from all its commercial plans in 2025 and placed multiple biosimilars on a preferred specialty tier (Tier 3). That means patients pay 25% coinsurance instead of 33%. That’s a real financial incentive. It’s not about fairness-it’s about profit. PBMs make money by steering patients toward cheaper drugs they negotiate discounts on. If biosimilars cost less, and the insurer gets a bigger rebate, they’ll push them hard.

But here’s the irony: this only works if the biosimilar is actually covered. And even then, many patients don’t know they’re being steered. A patient might get a letter saying their Humira is no longer covered, and they must switch. No discussion. No choice. Just a new prescription.

The Real Cost to Patients

The Medicare Rights Center found that when biosimilars and reference biologics are on the same tier, patients pay nearly the same out-of-pocket cost. That’s not a savings-it’s a trap. If you’re paying $1,200 a month for Humira and $1,150 for a biosimilar, you’re not saving much. But you are risking disruption. You’re risking side effects from switching. You’re risking delays.And for patients on Medicare, the gap is worse. Many hit the coverage gap-the donut hole-after spending $5,000 out of pocket. With biologics, that can happen in just two months. Switching to a biosimilar might delay hitting the gap by a few weeks, but without lower-tier placement, it’s not enough.

What’s Changing in 2025?

The government is starting to notice. In late 2024, the Office of Inspector General (OIG) released a report that called current formulary practices “anti-competitive.” The FTC filed legal briefs arguing that PBMs and drugmakers were colluding to delay biosimilar adoption. And CMS, under pressure, now requires insurers to report how they cover biosimilars.Some progress is visible. In 2024, 78% of Medicare Part D plans included at least one biosimilar alongside the original drug. That’s up from 62% in 2023. But the real change is coming from PBMs, not policy. Express Scripts, OptumRx, and CVS Caremark are now excluding originator drugs to force biosimilar use. That’s not patient-first-it’s cost-first. But it’s working.

By 2027, experts predict biosimilars will capture 40% of the market, up from just 23% today. Europe already has 80% adoption. Why? Because their insurers put biosimilars on lower tiers, waived prior authorization, and didn’t require step therapy. The U.S. is catching up, but slowly.

What You Can Do

If you’re on a biologic and your insurance won’t cover the biosimilar:- Ask your doctor to submit a letter of medical necessity-explain why switching could harm you.

- Call your insurer and ask: “Is the biosimilar on a lower tier than the reference product?” If not, file a formal appeal.

- Check if your plan has a biosimilar transition program. Some offer free trials or co-pay assistance.

- Use tools like the Center for Biosimilars formulary database to see what’s covered in your state.

And if you’re a provider: track your prior authorization success rates. If you’re spending hours on denials, push your clinic to hire a dedicated prior auth specialist. It’s not just paperwork-it’s patient care.

Bottom Line

Biosimilars are here. They’re safe. They’re cheaper. But insurance rules are still designed to protect the status quo. Until insurers stop putting biosimilars on the same tier as the original drug, or stop requiring prior authorization that’s just as strict, patients will keep paying high prices for drugs that could save them money. The system isn’t broken-it’s being manipulated. And until that changes, the savings will stay locked away.Why aren’t biosimilars on lower insurance tiers if they’re cheaper?

Most insurers place biosimilars on the same tier as the original biologic because the drugmakers and pharmacy benefit managers (PBMs) still have financial agreements in place. Even though biosimilars cost less, the original manufacturer may offer rebates to the PBM if the drug stays on the formulary. This creates no financial incentive for the insurer to move the biosimilar to a lower tier. As a result, patients see little to no out-of-pocket savings when switching.

Can my pharmacist switch me to a biosimilar without my doctor’s approval?

Only if the biosimilar is designated as "interchangeable" by the FDA. As of 2025, only a handful of biosimilars have this status-and even then, it applies to very specific formulations. For example, one interchangeable adalimumab biosimilar exists, but only for the low-concentration version of Humira. Most biosimilars are not interchangeable, so your pharmacist cannot substitute them without your doctor’s explicit order.

What’s the difference between a biosimilar and a generic drug?

Generics are exact chemical copies of small-molecule drugs, like aspirin or metformin. Biosimilars are made from living cells and are "highly similar" to their reference biologic, but not identical. Because they’re complex proteins, they can’t be copied exactly. However, they must meet strict FDA standards proving they work the same way with no meaningful difference in safety or effectiveness.

Why do some insurers refuse to cover any biosimilars at all?

Some insurers, especially in 2023-2024, kept biosimilars off formularies because the original drug manufacturers offered them financial incentives to exclude competitors. These rebates were sometimes tied to volume guarantees. Even after biosimilars entered the market, insurers kept the original drug on formulary to keep getting those payments. Starting in 2025, some PBMs are reversing this by excluding the original drug entirely to force use of biosimilars-where they can negotiate better discounts.

How long does prior authorization for a biosimilar usually take?

It typically takes between 3 and 14 business days. Some insurers process it faster if the prescriber submits complete documentation-like lab results, prior treatment failures, and a letter explaining medical necessity. Delays often happen when insurers request additional records or when the patient is being forced through step therapy. In urgent cases, doctors can request an expedited review, which should be decided within 72 hours.

Are there any programs to help pay for biosimilars if insurance denies coverage?

Yes. Many biosimilar manufacturers offer patient assistance programs, including co-pay cards and free trial supplies. Some nonprofit organizations, like the Arthritis Foundation and Patient Access Network Foundation, also help eligible patients with out-of-pocket costs. Always ask your pharmacist or doctor about these programs-many patients don’t know they exist.

For patients on biologics, the path to affordable care is still tangled. But awareness is growing. As more insurers shift toward exclusionary formularies and CMS tightens oversight, the system may finally start working for patients-not just profits.

Milad Jawabra

March 4, 2026 AT 09:00Yo this is wild. I’ve been on Humira for 5 years and my insurer just dropped the biosimilar last month. Said I had to "try the original first" like it’s a damn game of musical chairs. I’m paying $1,200/month while my buddy in Canada pays $120 for the same drug. What the actual fuck is wrong with this system? 🤬

Chris Beckman

March 4, 2026 AT 09:22so biosimilars are like generics but not really? i always thought they were exact copies. guess i was wrong. also why do insurers care if its a biosimilar or not if its cheaper? theyre supposed to save money right? this whole thing is just bs. i dont get it

Levi Viloria

March 5, 2026 AT 02:39It’s funny how the system works. PBMs aren’t evil-they’re just following the money. If a drugmaker gives them a rebate for keeping Humira on the formulary, they’ll do it. No malice, just economics. But when you’re the one paying $1,200 out of pocket, it doesn’t feel like economics. It feels personal. And honestly? It should.

Richard Elric5111

March 6, 2026 AT 09:10One must interrogate the ontological underpinnings of pharmaceutical capitalism as it pertains to biosimilar adoption. The current paradigm, predicated upon the commodification of biological therapeutics, is not merely inefficient-it is epistemologically incoherent. The FDA’s regulatory framework, while rigorous, fails to account for the hermeneutic gap between clinical equivalence and economic accessibility. Consequently, the patient becomes an epiphenomenon in a system designed to maximize shareholder value, not therapeutic outcomes.

Dean Jones

March 7, 2026 AT 11:53Let’s be real. The whole biosimilar mess isn’t about science. It’s about who controls the levers. Drugmakers used to have a monopoly on Humira. Now they’re losing it. So they cut deals with PBMs to keep their product on formularies-even when cheaper, equally effective alternatives exist. And PBMs? They’re not villains. They’re just profit-maximizing middlemen who don’t give a shit about you unless you’re a line item on their quarterly report. The fact that we’ve had 70+ approved biosimilars since 2015 and still only 40 are on the market? That’s not a regulatory failure. That’s a collusion failure. And it’s going to take a federal crackdown, not patient advocacy, to fix it.

Betsy Silverman

March 7, 2026 AT 23:34I’m a nurse and I see this every day. Patients crying because they can’t afford their meds. One lady had to choose between her Humira and her insulin. She picked insulin. Her RA flared. She couldn’t work. We had to call social services. This isn’t healthcare. It’s a financial obstacle course. We need tiered biosimilar coverage. Now. Not in 2027. Now.

Helen Brown

March 8, 2026 AT 21:20you think this is bad? wait till you find out the FDA and big pharma are in cahoots. biosimilars are secretly less safe. they inject nanobots to track you. the government wants to control your immune system. you think your doctor is helping you? they’re just following orders. read the 2024 CDC memo. its hidden in plain sight.

John Cyrus

March 10, 2026 AT 08:33People dont understand that biosimilars arent actually the same. The FDA says they are but theyre not. You cant replicate a living cell. Its impossible. So why are we forcing people to switch? Its dangerous. And why are we letting PBMs decide what we take? Theyre not doctors. Theyre accountants. This is madness

Aisling Maguire

March 12, 2026 AT 03:28Irish here. We got biosimilars on Tier 1 here. No prior auth. No step therapy. Just walk in, get your script, pay €10. No drama. The US system is like a Kafka novel written by a greedy accountant. How are you still like this?!

marjorie arsenault

March 13, 2026 AT 07:45Hey, if you’re struggling with this-reach out. I’ve helped 3 people get co-pay assistance this month. There are programs. They’re not perfect, but they exist. Your doctor might not know about them. Your pharmacist might not mention them. But I’ll send you the links if you DM me. You’re not alone. Seriously.

Deborah Dennis

March 15, 2026 AT 07:36Wow. Just… wow. So the system is rigged. The drug companies are evil. PBMs are greedy. Patients are pawns. And the government? Oh, they’re just "starting to notice." Like, after 10 years? What a surprise. I’m so glad we live in a country where profit > people. /s

Megan Nayak

March 17, 2026 AT 01:59You know what’s ironic? The same people who scream about "government overreach" when it comes to masks or vaccines are the ones defending insurance companies that block life-saving drugs. The system doesn’t care if you live or die. It cares about margins. And if you think this is about healthcare? You’re not just naive-you’re complicit. Wake up. This isn’t a bug. It’s a feature.